Most of us have heard the Brand 'Eveready' and it's tag line 'Give me Red'. It has been the dominant player in the dry-cell batteries business for many many years now. It sells over 100 crore batteries every year. But not many have heard of Eveready Industries Ltd in the Stock Market world. The company was not doing much well on the Profit front until about 2 years ago. A couple of years ago, the younger generation of the Khaitan family took over the reigns of Eveready Industries Ltd. Since then the company has started expanding it's product portfolio & reducing it's dependence on the gradually-depleting batteries business.

( Click here for Eveready's Easy Results Summary page. )

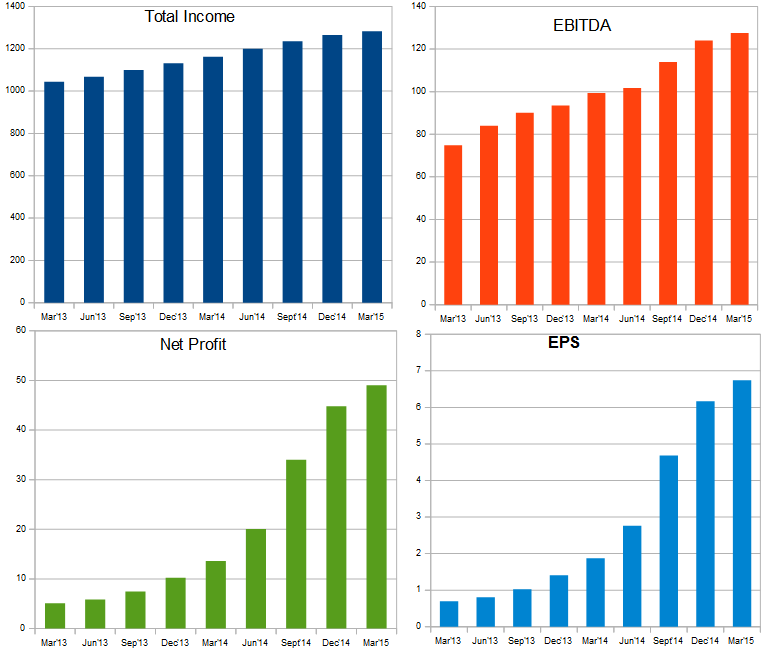

Over the last 2-3 years, Eveready Industries Ltd has launched many new products like Torch-lights, Rechargeable Flash-Lights and CFL bulbs. These newer products have helped the company expand it's Top-line by about 10-12% every year over the last 2-3 years to touch a figure of Rs.1283 crores for FY'15, despite the fact that the batteries business has been stagnating over the recent years. The Top-line growth has been quite moderate, but the bigger development has been the huge improvement in the Profitability. Have a look at the Trailing-Twelve-Month charts below to get a better idea:

Look at the T-T-M EBITDA & Net Profit charts. Eveready Industries Ltd has seen a sharp increase on these two parameters over the last 2 years and this is the highlight of the company's remarkable turnaround. Over the last 2 years, the company's EBITDA margins have improved by about 280 basis points to reach almost 10% now. Between FY'13 and FY'15, Eveready Industries' Total Income jumped by about 23%, but it's EBITDA grew by just over 70%, thanks to the expanded margin performance. Net Profit during the same period has multiplied nearly 10 times to just over Rs.49 crores. The Net Profit margin improved sharply from just 0.50% to 3.82% in the last 2 years. Apart from improvement in EBITDA, the company has managed to reduce it's Interest Cost by about 18% and Depreciation provisioning by about 25% in the last one year, which helped it improve margins sharply. This sharp improvement in profitability has clearly attracted investors attention and the stock has rallied more than 15 times from levels of about Rs.17-18 to a range of about Rs.260-280 currently. At these prices, the stock trades at about 40 times it's 12-months EPS, which is in-line with what other FMCG peers trade at, or even slightly higher.

Look at the T-T-M EBITDA & Net Profit charts. Eveready Industries Ltd has seen a sharp increase on these two parameters over the last 2 years and this is the highlight of the company's remarkable turnaround. Over the last 2 years, the company's EBITDA margins have improved by about 280 basis points to reach almost 10% now. Between FY'13 and FY'15, Eveready Industries' Total Income jumped by about 23%, but it's EBITDA grew by just over 70%, thanks to the expanded margin performance. Net Profit during the same period has multiplied nearly 10 times to just over Rs.49 crores. The Net Profit margin improved sharply from just 0.50% to 3.82% in the last 2 years. Apart from improvement in EBITDA, the company has managed to reduce it's Interest Cost by about 18% and Depreciation provisioning by about 25% in the last one year, which helped it improve margins sharply. This sharp improvement in profitability has clearly attracted investors attention and the stock has rallied more than 15 times from levels of about Rs.17-18 to a range of about Rs.260-280 currently. At these prices, the stock trades at about 40 times it's 12-months EPS, which is in-line with what other FMCG peers trade at, or even slightly higher.

What's in store in the future? A few months ago Eveready Industries Ltd has aggressively entered the fast-growing business of LED bulbs. It is sourcing it's supplies from China under contract manufacturing currently. For FY'15, 20% of the company's revenues came from the Lighting products business, including CFLs, LEDs, Torchlights and Flashlights. Riding in the fast acceptance of LED bulbs from Urban consumers and expected surge in demand from rural areas with prices expected to fall sharply in the coming months, Eveready Industries expects to see a huge surge in demand for LEDs in the coming quarters & years. The expects to triple it's revenues from the Lighting products business over the next 2-3 years. The company is even planning to launch some new products like Rechargeable Fans, etc. in the coming months. This expected surge in revenues from Lighting products and other non-battery business is expected to enable the company to post a decent growth of 12-15% Y-o-Y for the next 2-3 years. The Profit growth could be better than the revenue growth as there is still some scope for margin improvement that the company can manage with increasing scale of operations of these newer products.

Valuations are already on the expensive side and are so only because of the huge improvement the company has reported in it's profitability. If the company does disappoint on this front in the coming quarters, then we could see some sharp fall in it's stock price. So please be warned on this point. But if the company does continue with it's improved margins and push it little more higher, then the stock can comfortably command the P/E multiple in excess of 35.

( Click here for Eveready's Easy Results Summary page. )

Over the last 2-3 years, Eveready Industries Ltd has launched many new products like Torch-lights, Rechargeable Flash-Lights and CFL bulbs. These newer products have helped the company expand it's Top-line by about 10-12% every year over the last 2-3 years to touch a figure of Rs.1283 crores for FY'15, despite the fact that the batteries business has been stagnating over the recent years. The Top-line growth has been quite moderate, but the bigger development has been the huge improvement in the Profitability. Have a look at the Trailing-Twelve-Month charts below to get a better idea:

What's in store in the future? A few months ago Eveready Industries Ltd has aggressively entered the fast-growing business of LED bulbs. It is sourcing it's supplies from China under contract manufacturing currently. For FY'15, 20% of the company's revenues came from the Lighting products business, including CFLs, LEDs, Torchlights and Flashlights. Riding in the fast acceptance of LED bulbs from Urban consumers and expected surge in demand from rural areas with prices expected to fall sharply in the coming months, Eveready Industries expects to see a huge surge in demand for LEDs in the coming quarters & years. The expects to triple it's revenues from the Lighting products business over the next 2-3 years. The company is even planning to launch some new products like Rechargeable Fans, etc. in the coming months. This expected surge in revenues from Lighting products and other non-battery business is expected to enable the company to post a decent growth of 12-15% Y-o-Y for the next 2-3 years. The Profit growth could be better than the revenue growth as there is still some scope for margin improvement that the company can manage with increasing scale of operations of these newer products.

Valuations are already on the expensive side and are so only because of the huge improvement the company has reported in it's profitability. If the company does disappoint on this front in the coming quarters, then we could see some sharp fall in it's stock price. So please be warned on this point. But if the company does continue with it's improved margins and push it little more higher, then the stock can comfortably command the P/E multiple in excess of 35.

No comments:

Post a Comment