Reliance Power had another steady quarter with Total Income growing by 20% Y-o-Y during Q4. EBITDA was higher by 33.6%, thanks to higher margins from lower fuel cost. But the Cash Profit was higher only by 15.5% mainly because of 57.5% increase in Interest Cost. 62% higher Depreciation provisioning and 70% higher Tax outgo meant that the Net Profit was nearly flat with less than 3% growth.

( Click here of Reliance Power's Easy Results Summary page. )

Remember that Reliance Power has not started consolidating revenue & profit numbers from 3960 MW Sasan UMPP and the new 100 MW Concentrated Solar Power plant in Rajasthan. Most probably this will start from Q1 on this fiscal. During FY'15, Reliance Power generated & sold a total of 1239 crore units of electricity from it's 4 active projects: 1200 MW Rosa plant in UP, 600 MW Butibori plant in Maharashtra, 40 MW Solar plant again in Rajasthan and 45 MW Wind project in Maharashtra. Total Revenues for the year stood at Rs.7202 crores, translating into an average rate of Rs.5.80 per unit of electricity sold by Reliance Power. This average rate number will drop sharply as soon as the numbers from Sasan UMPP start getting consolidated because the selling rate for units from that project is just about Rs.1.20-1.30 per unit.

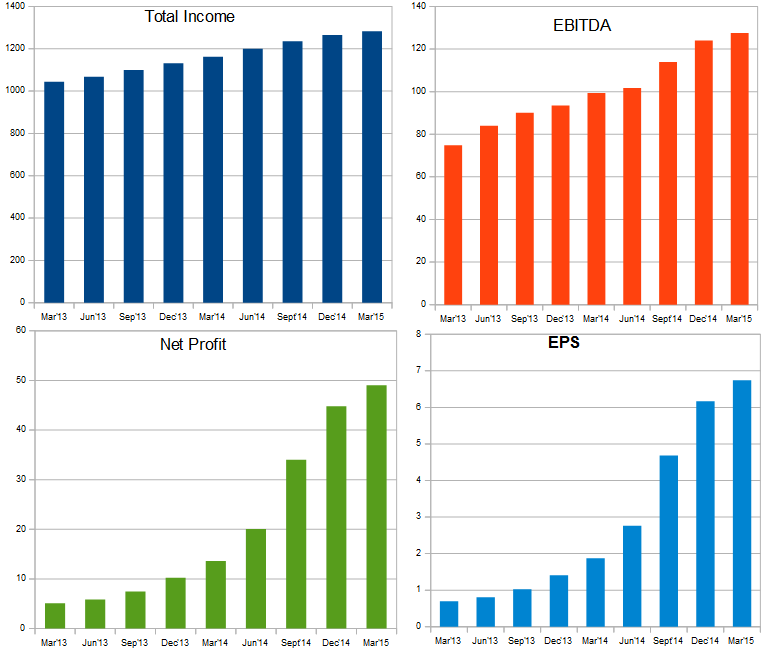

Have a look at the Trailing-Twelve-Months charts alongside. The Total Income & EBITDA was quite stable between March'13 to March'14. Then the Butibori project numbers started getting consolidated from June'14 and hence the Total Income & EBITDA started going up noticeably. The Cash Profit grew at a slower rate mainly because of the sharp increase in the Interest Cost from June'14 quarter onwards. IF no new project was to get commissioned now, the charts would again have stabilised. But we are expecting Sansan UMPP and the 100 MW CSP in Rajasthan to start adding to RPower's numbers from June'15 quarter onwards. So the upswing in the charts is expected to continue. Infact the upmove in Total Income chart could be stronger than last year. EBITDA & Cash Profit growth might be moderate, depending on the profitability of the Sasan project.

Have a look at the Trailing-Twelve-Months charts alongside. The Total Income & EBITDA was quite stable between March'13 to March'14. Then the Butibori project numbers started getting consolidated from June'14 and hence the Total Income & EBITDA started going up noticeably. The Cash Profit grew at a slower rate mainly because of the sharp increase in the Interest Cost from June'14 quarter onwards. IF no new project was to get commissioned now, the charts would again have stabilised. But we are expecting Sansan UMPP and the 100 MW CSP in Rajasthan to start adding to RPower's numbers from June'15 quarter onwards. So the upswing in the charts is expected to continue. Infact the upmove in Total Income chart could be stronger than last year. EBITDA & Cash Profit growth might be moderate, depending on the profitability of the Sasan project.

Since the selling price of power produced at Sasan UMPP is very low, the impact of RPower's Topline is not going to be as big as the Project's generation capacity suggests. This one project is tripling RPower's active Generation capacity from little under 2000 MW to little under 6000 MW. But Revenue growth is not going to be 200%. It will be around 50%. If Sasan project runs around the 85-90% PLF levels, then the Income from this project for the year could be in the region of Rs.2800 to 3200 crores. Since the Coal mine is linked to the project, the Fuel purchase cost will be zero. Only the cost of mining the coal & other operating costs will be included. I am expecting all the operating & non-operating costs for this project to be around Rs.700-800 crores, which will translate into very high EBITDA margins. Interest Cost is expected to increase by around Rs.1500-1800 crores. That means the Cash Profit should grow by about Rs.300 to 500 crores over the year. But the Net Profit of RPower could drop from current levels, because the Depreciation provisioning for Sasan UMPP is expected to be high at about Rs.900-1000 crores every year.

The number above are just rough estimates that I had in my mind. In terms of quarterly numbers, we could see RPower report a Total Income figure of around Rs.2300 to 2500 crores, once Sasan numbers are added. EBITDA could jump to about Rs.1275 to 1300 crores. Cash Profit could be around Rs.500 to 550 crores. Net Profit could drop to about Rs.100 crores. If there is no major further CAPEX immediately, the company can use the Cash Profits to start repaying the loans, which will bring down the Interest Costs and improve the Net Profits. But if the company has further projects to spend on, then the Cash Profits will get utilised there. Let's see. RPower's numbers are expected to grow and the growth is Cash Flow positive. That's the important thing.

Over the recent couple of months, Reliance Power's stock has got further corrected to levels under Rs.55/-, translating into a Market Cap of just about Rs.15,000 crores. This is very very cheap valuations. The company is expected to generate Cash Profits of over Rs.2000 crores in FY'16. That means it is trading at just about 7 times it's expected Cash Profit, which is very low. There is substantial scope for the stock to get re-rated higher in the coming months, unless there is some ugly surprise in the numbers in the coming quarter or two. But I don't think that's going to happen. I am positive on Reliance Power and expect the stock to a range of Rs.75 to 90 anytime over the next 12 months.

( Click here of Reliance Power's Easy Results Summary page. )

Remember that Reliance Power has not started consolidating revenue & profit numbers from 3960 MW Sasan UMPP and the new 100 MW Concentrated Solar Power plant in Rajasthan. Most probably this will start from Q1 on this fiscal. During FY'15, Reliance Power generated & sold a total of 1239 crore units of electricity from it's 4 active projects: 1200 MW Rosa plant in UP, 600 MW Butibori plant in Maharashtra, 40 MW Solar plant again in Rajasthan and 45 MW Wind project in Maharashtra. Total Revenues for the year stood at Rs.7202 crores, translating into an average rate of Rs.5.80 per unit of electricity sold by Reliance Power. This average rate number will drop sharply as soon as the numbers from Sasan UMPP start getting consolidated because the selling rate for units from that project is just about Rs.1.20-1.30 per unit.

Since the selling price of power produced at Sasan UMPP is very low, the impact of RPower's Topline is not going to be as big as the Project's generation capacity suggests. This one project is tripling RPower's active Generation capacity from little under 2000 MW to little under 6000 MW. But Revenue growth is not going to be 200%. It will be around 50%. If Sasan project runs around the 85-90% PLF levels, then the Income from this project for the year could be in the region of Rs.2800 to 3200 crores. Since the Coal mine is linked to the project, the Fuel purchase cost will be zero. Only the cost of mining the coal & other operating costs will be included. I am expecting all the operating & non-operating costs for this project to be around Rs.700-800 crores, which will translate into very high EBITDA margins. Interest Cost is expected to increase by around Rs.1500-1800 crores. That means the Cash Profit should grow by about Rs.300 to 500 crores over the year. But the Net Profit of RPower could drop from current levels, because the Depreciation provisioning for Sasan UMPP is expected to be high at about Rs.900-1000 crores every year.

The number above are just rough estimates that I had in my mind. In terms of quarterly numbers, we could see RPower report a Total Income figure of around Rs.2300 to 2500 crores, once Sasan numbers are added. EBITDA could jump to about Rs.1275 to 1300 crores. Cash Profit could be around Rs.500 to 550 crores. Net Profit could drop to about Rs.100 crores. If there is no major further CAPEX immediately, the company can use the Cash Profits to start repaying the loans, which will bring down the Interest Costs and improve the Net Profits. But if the company has further projects to spend on, then the Cash Profits will get utilised there. Let's see. RPower's numbers are expected to grow and the growth is Cash Flow positive. That's the important thing.

Over the recent couple of months, Reliance Power's stock has got further corrected to levels under Rs.55/-, translating into a Market Cap of just about Rs.15,000 crores. This is very very cheap valuations. The company is expected to generate Cash Profits of over Rs.2000 crores in FY'16. That means it is trading at just about 7 times it's expected Cash Profit, which is very low. There is substantial scope for the stock to get re-rated higher in the coming months, unless there is some ugly surprise in the numbers in the coming quarter or two. But I don't think that's going to happen. I am positive on Reliance Power and expect the stock to a range of Rs.75 to 90 anytime over the next 12 months.